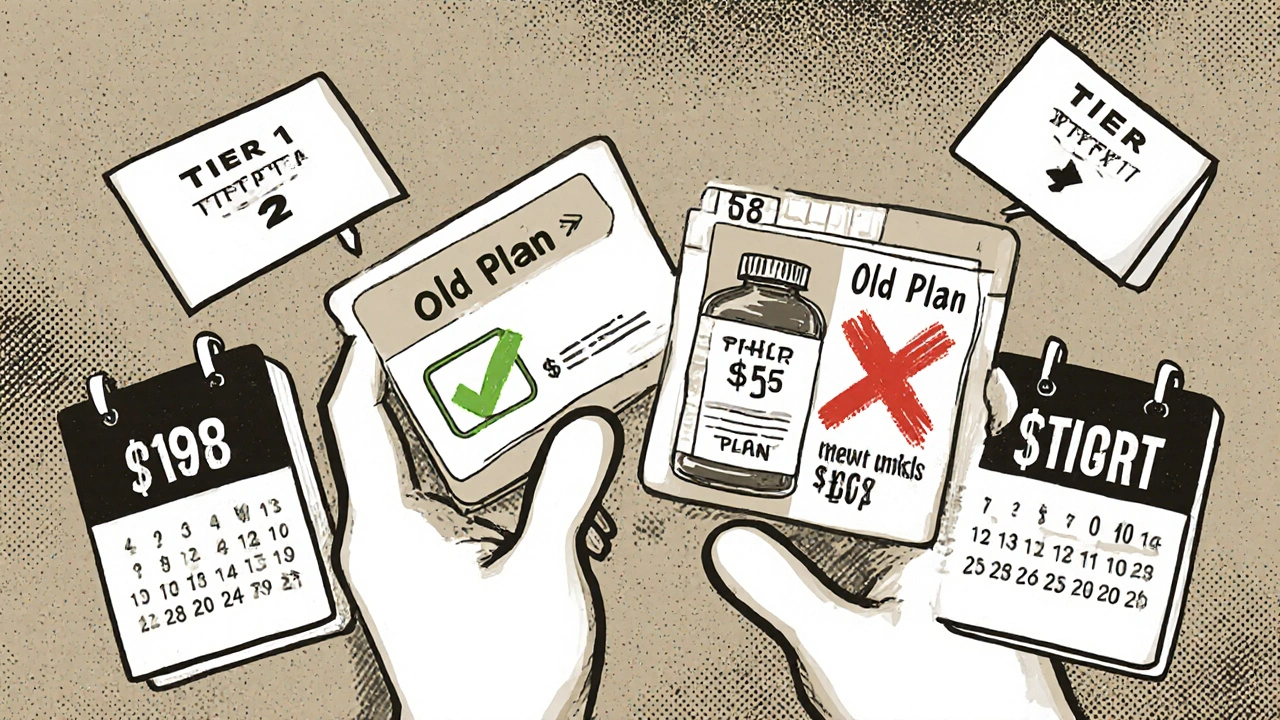

When you pick up a prescription, the price you pay isn’t just set by the drug company—it’s shaped by your insurance plan’s formulary tiers, a system that groups medications into cost levels based on price, effectiveness, and negotiation deals. Also known as drug formulary, it’s how pharmacies and insurers decide what you pay out-of-pocket for each pill or injection. You might not see it, but every time you swipe your card at the pharmacy, you’re hitting one of these tiers.

Most plans use four to five tiers. Tier 1 is usually generic drugs—cheap, effective, and preferred by insurers. Tier 2 is brand-name drugs with generic alternatives available. Tier 3 is higher-cost brand-name meds with no cheap version. Tier 4? That’s for specialty drugs, like those for cancer or MS, which can cost hundreds or even thousands per month. Some plans even have Tier 5 for the most expensive treatments. The kicker? The higher the tier, the more you pay. It’s not random—it’s designed to push you toward cheaper options. Insurers negotiate deals with drug makers to get lower prices on meds in lower tiers, then pass some of those savings to you. But if you pick a drug on Tier 4 or 5, you’re often stuck paying more unless you appeal or switch.

This system ties directly to how pharmacy benefit managers, companies that manage drug coverage for insurers and employers. Also known as PBMs, they decide which drugs go where on the formulary. They don’t just pick based on safety—they pick based on cost, rebates, and contracts. That’s why two plans with the same insurer might list different drugs on Tier 1. It’s also why some drugs you’ve used for years suddenly jump to a higher tier. You’re not imagining it. The formulary changed.

And it’s not just about price. Formulary tiers affect what your doctor prescribes. If your doctor wants to give you a brand-name drug on Tier 3, they might need prior authorization—meaning the insurer has to approve it before you get it. Sometimes, they’ll ask you to try a cheaper generic first. That’s called step therapy. It’s legal, common, and often frustrating. But knowing how tiers work lets you ask the right questions: Is there a generic? Can we try a Tier 1 alternative? What’s the cost difference?

What you’ll find below are real, practical guides that break down how this system impacts your daily life. You’ll read about how generic drugs get approved and priced, how to avoid absorption problems with common meds like calcium and bisphosphonates, and why some drugs like ramipril or tolvaptan come with strict diet rules. You’ll see how insurance formularies shape choices for everything from antidepressants to erectile dysfunction pills. These aren’t theoretical—they’re based on how real people navigate prescriptions, copays, and surprise bills.

When switching health plans, your generic drug coverage can save or cost you hundreds a year. Learn how formulary tiers, deductibles, and state rules impact your prescription costs-and how to avoid expensive surprises.

The best time to take statins isn't about night or morning-it's about consistency. Learn how statin timing affects side effects and cholesterol lowering, and why adherence beats clock time.

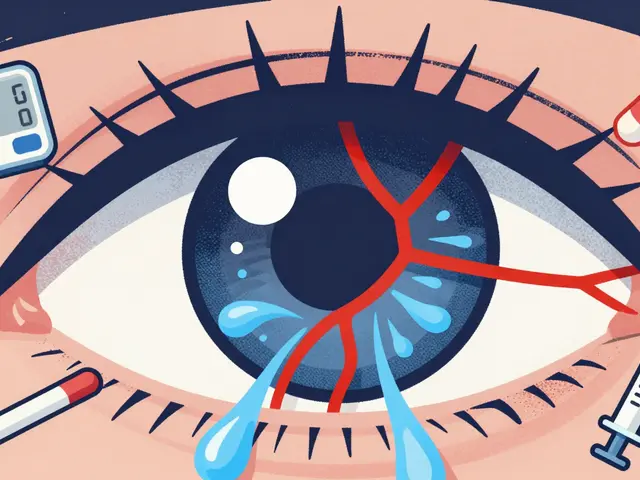

Retinal vein occlusion is a leading cause of sudden vision loss. Learn the key risk factors like high blood pressure and diabetes, and how anti-VEGF and steroid injections help restore vision. Understand treatment realities, costs, and what’s coming next.

Low-dose CT screening can save lives in smokers by catching lung cancer early. Learn who qualifies, how it works, the real risks, and what to do next.

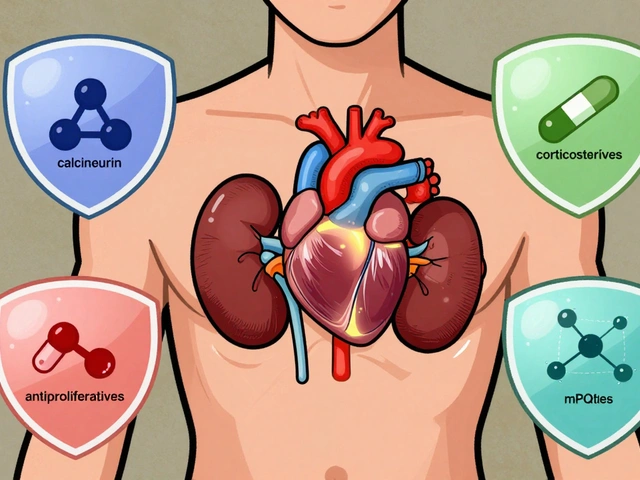

Immunosuppressants prevent organ rejection after transplant but carry serious risks like infection, cancer, and kidney damage. Learn how to manage these drugs safely, avoid missed doses, and reduce long-term side effects.

Dependence on foreign manufacturing for pharmaceutical ingredients is causing widespread drug shortages. With over 80% of active ingredients coming from just a few countries, disruptions in China or India directly impact patient access to life-saving medications.